The construction industry is once again facing a familiar challenge. Specifically, geopolitical conflicts translating directly into higher project costs, price volatility, and contractual disputes. The ongoing war involving Iran and the continuing disruptions to shipping traffic through the Strait of Hormuz have sent shockwaves through energy markets, international shipping, and construction supply chains worldwide.

For owners, contractors, developers, and lenders, these disruptions are no longer abstract global events. They are showing up in the form of escalating fuel prices, material price increases, procurement delays, and shrinking profit margins.

Why the Strait of Hormuz Matters to Construction

The Strait of Hormuz is the primary shipping route for approximately 20–25% of the world’s oil supply, along with major volumes of liquefied natural gas, petrochemicals, aluminum, steel inputs, and fertilizers. Since late February 2026, military operations between the United States, Israel, and Iran have led to a near standstill of routine commercial traffic through the Strait.

Energy markets reacted immediately. Oil prices shot to above $100 per barrel in March and April 2026, with U.S. gasoline and diesel prices increasing more than 40% in a matter of weeks. Because fuel is a foundational input for virtually every construction activity (e.g., manufacturing, transportation of materials, on‑site equipment operation, etc.) these increases rapidly affect project budgets.

Impact on Construction Materials and Supply Chains

Fuel and Freight

The most immediate and visible impact to the construction industry has been fuel driven cost escalation. Spikes in diesel costs are being absorbed by suppliers, freight carriers, and subcontractors, pushing up the cost of delivered materials even when underlying commodity prices remain stable. The closure of the Strait of Hormuz has added to these pressures by forcing many vessels to reroute around the Cape of Good Hope. These detours add thousands of miles, require substantially more fuel, and can extend transit times by up to two weeks for cargo coming from Asia. As a result, freight costs have increased significantly, and projects already operating on tight schedules are experiencing additional delivery delays.

Steel, Aluminum, Cement, and Energy‑Intensive Materials

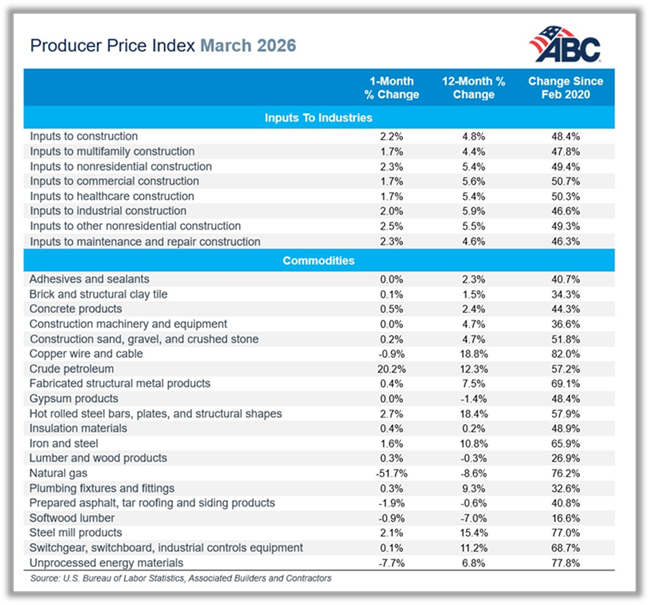

The pricing of many core construction materials are especially volatile because of their energy‑intensive production processes. For instance, steel, aluminum, and cement require large volumes of natural gas and/or electricity for manufacture and transportation to jobsites. The prices of these materials have already risen in reaction to the Iran conflict. U.S. construction producer price indexes show month‑over‑month increases of more than 2% for steel products and .5% for concrete products since early the beginning of February 2026, with further increases anticipated if disruptions persist.

Lead Times and Availability

Beyond price, schedule risk is increasing. Suppliers are expected to experience longer lead times due to disrupted shipping, insurance constraints, and port congestion at alternative routes. Even where materials remain available, suppliers are going to be increasingly reluctant to hold pricing beyond very short validity periods, which will complicate bidding, procurement, and financing decisions.

Legal and Contractual Considerations

From a construction law perspective, the current geopolitical environment underscores the importance of careful contract drafting to mitigate risk and allocate responsibility for events outside a party’s control. Owners, contractors, and subcontractors should pay particular attention to provisions addressing unforeseen disruptions and cost volatility.

- Force majeure clauses: A force majeure clause excuses or delays performance when extraordinary events beyond a party’s reasonable control prevent or hinder that performance. Well‑drafted force majeure provisions may account for geopolitical conflicts, war, government actions, or disruptions to transportation networks. When properly structured, these provisions can provide relief from default or delay damages where global conflicts affect material procurement, labor availability, or logistics.

- Price escalation provisions: Price escalation provisions allow contract prices to be adjusted in response to significant and unforeseen increases in material, fuel, or freight costs. Given the recent volatility in energy markets and supply chains, escalation clauses tied to objective indices or documented cost increases can help equitably distribute risk and prevent parties from absorbing unsustainable losses or abandoning projects altogether.

- Fuel escalation clauses: Fuel escalation clauses are a specific type of price adjustment mechanism that ties contract pricing to fluctuations in fuel costs, typically tied to a published fuel pricing index. When fuel prices exceed a contractually defined threshold, the clause triggers an automatic adjustment to the contract price, allowing the affected party to recover the additional cost without the need to renegotiate. These provisions protect contractors and subcontractors from absorbing sudden and dramatic increases in fuel costs that were unforeseeable at the time of bid or contract execution.

- Excusable delay provisions: Excusable delay provisions address circumstances where performance is delayed due to events outside a contractor’s control, entitling the contractor to schedule relief without exposure to liquidated damages. Disruptions caused by war‑related shipping delays, material shortages, or port congestion may qualify as excusable delays if properly defined and supported by notice and mitigation requirements in the contract.

Collectively, these contractual protections can help construction industry participants minimize the impact of the anticipated wave of litigation related to the war in Iran.

Looking Ahead

Even if active hostilities subside, there is always risk of continued pricing volatility. Shipping traffic through the Strait of Hormuz remains far below pre‑war levels, and pricing is unlikely to normalize quickly. For the construction industry, this means that cost pressure may persist well into 2026 and beyond.

Owners and contractors should therefore reassess their pricing assumptions, contractual risk allocation, and procurement strategies in light of ongoing geopolitical tensions. Recent history has shown that construction industry participants who proactively address global disruption risks through thoughtful contract drafting and planning are far better positioned to withstand these events, which appear to be occurring with increasing frequency.

[View source.]